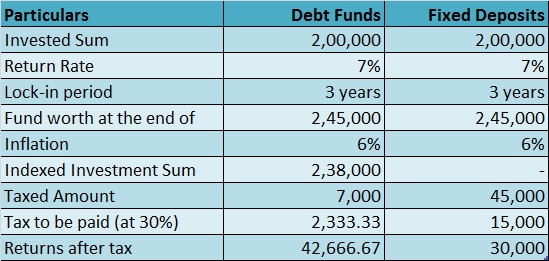

You must add the short-term debt fund gains (less than 3 years) to your income and they are taxable as per your tax slab rate. For long-term gains, there is a 20% after the indexation benefits. As for fixed deposit returns, you can add it to your income and it will be taxed accordingly.

The main difference between this two low-risk investment instruments is that of taxation.

In case of Fixed Deposits (FD)

The interest earned from FDs is added to your annual income for taxation purposes. Hence, the tax rate on interest earned from FDs will depend on your income tax slab, i.e. 5 %, 20 % or 30 % on the interest received.

For example, if your annual income, after including interest earned from your FDs, falls within the 30% tax bracket, the interest component will attract 30% income tax. Since many investors are in the top tax bracket, this takes away a large chunk of their returns.

In case of Debt Funds

Taxes upon debt mutual funds are of two types depending upon the period for which they are held. These two types are:

Short-term Capital Gain Tax: This is applicable to debt mutual funds held for a period of 36 months or less i.e. anything less than 3 years. In short-term capital gain tax, tax on funds is calculated as per income tax slab of the individual, i.e. 5%, 20% or 30% on the amount of gain.

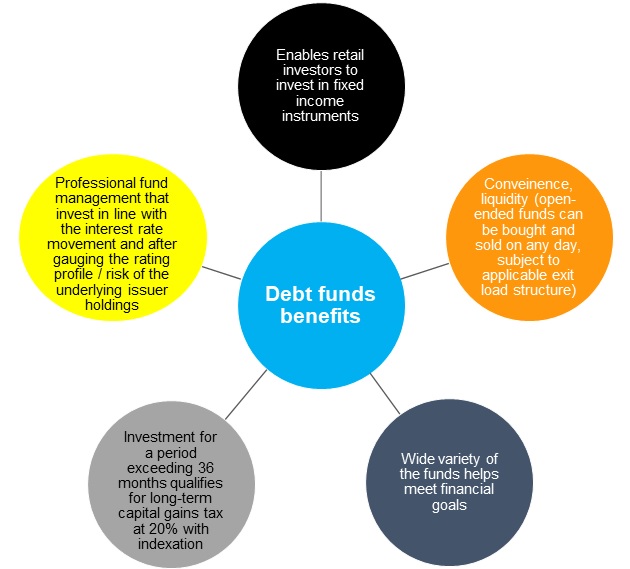

Long-term Capital Gain tax: This is applicable to debt mutual funds held for a period of 36 months or more i.e. anything more than 3 years. In long-term capital gain tax, tax on funds is calculated at the rate of 20 % with cost indexation on the amount of gain.

Tax Deducted at Source (TDS)

Apart from above mention taxation, banks also deduct TDS on interest income from fixed deposits. It was introduced to collect tax at the source from where an individual’s income is generated.

As per the Income Tax Act, any company or person making a payment is required to deduct tax at source if the payment exceeds certain threshold limits. TDS has to be deducted at the rates prescribed by the tax department.

As a resident Indian, there will be no TDS when you sell/redeem your debt fund units. You are required to show the income and pay taxes, if any when you file your returns.